Common steps required by foreign investors to establish a business in KSA in respect of healthcare services.

Christina SochackiSenior Counsel, Head of Healthcare & Life Sciences - Saudi Arabia

Hamed MatawiTrainee Lawyer,Corporate Commercial

The Kingdom of Saudi Arabia ("KSA”), as part of its recent Vision 2030 initiative, has been amending its laws and regulations with the aim to becoming a worldwide business hub for foreign investments. As part of these recent updates, the permissibility of foreign ownership in the healthcare sector has been expanded and a number of business vehicles are available to foreign investors seeking to operate in KSA.

In this article, we highlight the common steps required by foreign investors to establish a business in KSA, the common forms of business vehicles, and an overview of the foreign ownership restrictions and requirements in respect of healthcare services.

There are a number of common steps required to establish a business vehicle in KSA, regardless of the legal form, including the following:

registration with and obtaining an investment licence from the Ministry of Investment Saudi Arabia (“MISA”). There are several types of investment licenses in order to operate in KSA, which are based on the Company’s activities, (i.e. manufacturing, services, trading, and professional licenses);

registration with and obtaining a Commercial Registration (“CR”) from the Ministry of Commerce (“MOC”);

obtaining all relevant additional licences and approvals required to carry out the business’ operations, such as from the Ministry of Health (if applicable); and

completion of the secondary registrations of the entity with all relevant KSA authorities (such as the General Organization for Social Development, Ministry of Human Resources and Social Development, etc.)

The most common types of business vehicles in KSA are as follows:

1. Limited Liability Company:A limited liability company (“LLC”) can be established and it is the most common form used by foreign investors in Saudi Arabia. One of the steps in forming an LLC will be approval of the draft Articles of Association of the company (“AOA”); referred to as Bylaws for single shareholder LLCs as per the New KSA Companies Law, issued by Royal Decree No. M/132 dated 01/12/1443H (“Companies Law”) enforced starting 18/01/2023, their notarisation by the competent KSA Notary Public, and publication.

Regulatory Filing and Management of the LLC:For completeness, we note that LLC(s) are required, on an annual basis, to file copies of the management's report (which covers the company's business, its financial position and the management's suggestion regarding the distribution of profits), the auditor's report, and audited financial statements with MOC. These documents need to be prepared within three months from the end of the financial year and filed within one month of preparation. Therefore, the MOC will be informed with respect to the utilization of the share capital amount. The MOC may make inquiries, in the event that the share capital amount is used for purposes other than the operation of the LLC.

The LLC can be managed by a single General Manager, two General Manager(s) or a Board of Directors. It would also be permissible for the LLC to be managed by both a General Manager and a Board of Directors.

Generally speaking, the Companies Law is virtually silent with respect to the requirements for the nomination and appointment of a Director and/or General Manager. The following requirements (generally) should be met:

The nominated person should be at least 18 years old; and

The nominated person should not be a governmental officer (in KSA) or an undischarged bankrupt individual pursuant to a court order.

Furthermore, one of the members of the Board of Directors (if the LLC is managed by a Board of Directors) or the General Manager (if the LLC is managed by a General Manager) must be a KSA resident. In other words, one member from the management of the LLC must be a KSA resident for the LLC to be fully operational (for Chamber of Commerce purposes and for being the signatory for the LLC's local bank account, for example).

2. Branch of a Foreign Company (“Branch”):It is possible to establish a branch of company that carries out the same business activity of the mother company. The formation process is generally similar to that of an LLC, except that the branch will not have separate AOA.

The main feature of a branch is that it is not a separate legal entity from the parent company and therefore it does not have a separate financial liability. The mother company will be liable for any debts incurred by the branch. Additionally, the branch will only be licensed to carry out the activities that the parent company is licensed to carry out.

3. Joint Stock Company:A Joint Stock Company (“JSC”) may be established under most circumstances. JSC may be listed or unlisted. However, it should be noted that after the incorporation of a listed JSC it will be regulated by the Capital Market Authority. The minimum capitalization of a JSC is five hundred thousand Saudi Riyal (SAR 500,000).

Regulatory Filing and Management of the JSC:JSC(s) are required, on an annual basis, to hold at least one Ordinary General Assembly, which would include the approval of the auditor's report and audited financial statements and the approval of the management report and other matters as deemed necessary by the JSC.

The permissibility of foreign ownership in the healthcare sector has been expanded and a number of business vehicles are available to foreign investors seeking to operate in KSA.

Further, the JSC(s) must be managed by a Board of Directors containing at least three directors; such directors are appointed by the general assembly of the JSC and any stockholder can nominate him/herself. The appointment of directors is for three years period with the possibility of re-election for unlimited periods. However, the general assembly of the JSC can remove the directors, unless stated otherwise in the bylaws of the JSC.

The JCS(s) can have a Managing Director, who can carry out the day to day operation and with his or her authorities stated in the bylaws, if applicable. Otherwise the Managing Director can be appointed through a Board resolution.

4. Other Business Models in KSA:In KSA, franchising is not considered a business vehicle, where the business is physically operating in KSA. If the entity would like to have a direct operation and existence in KSA, it will be required to operate through one of the abovementioned business vehicles. For completeness, we note that franchising under the new KSA Franchise Law, introduced in April 2020, Article (1) defines franchising as:

“an arrangement under which a Franchisor grants the Franchisee the right to conduct a business – the subject matter of the Franchise – for its own account in association with a trademark or tradename, owned by or licensed to the Franchisor and includes the provision to the Franchisee of technical expertise and know-how and determining the manner in which the business is to be operated; in return for cash or non-cash consideration, other than amounts paid by the Franchisee to the Franchisor in consideration of the goods or services so provided”.

It is worth noting that, if an entity is not legally established in KSA, it may not conduct business in the KSA jurisdiction.

We note that in KSA, the authorities have recently become more proactive concerning issues with concealment (businesses that operate illegally under a third party local entity, without legal existence in KSA). While it is common place in the UAE to have side agreements conveying beneficial interest in shares to third parties who are not registered on the commercial register as legal shareholders, investors beware in Saudi; such arrangements are prohibited. Foreign entities that have a foreign (non-GCC) shareholder will be considered foreign-owned companies and subject to foreign ownership restrictions and other licensing and compliance requirements.

Concealment is deemed a breach of the KSA foreign investment law (in addition to several other laws and regulations). Typical violations of Saudi anti-concealment Law include:

A non-Saudi investing in a corporate entity with activities that are restricted to wholly Saudi owned companies, without disclosing such foreigner ownership/investment to the Saudi government;

A foreign businesses establishing commercial operations in Saudi without first obtaining a foreign investment licence; and

Similar “fronting arrangements” such as nominee arrangements whereby the ultimate beneficiary is a non-Saudi national who did not obtain a foreign investment licence to carry out the business in Saudi Arabia, but nevertheless does through their Saudi partner who legally holds all of the shares in the business.

Additionally, with regards to employment and man-labour in KSA, not setting up any legal entity would restrict the foreign entity from employing any employees in KSA, noting that in order to have employed (operating) persons in KSA, the KSA labour law requires that the employer must have a legal establishment in KSA in order to register their employees to the required secondary registrations

(i.e. General Organization for Social Development, Ministry of Human Resources and Social Development, Muqeem, etc.).

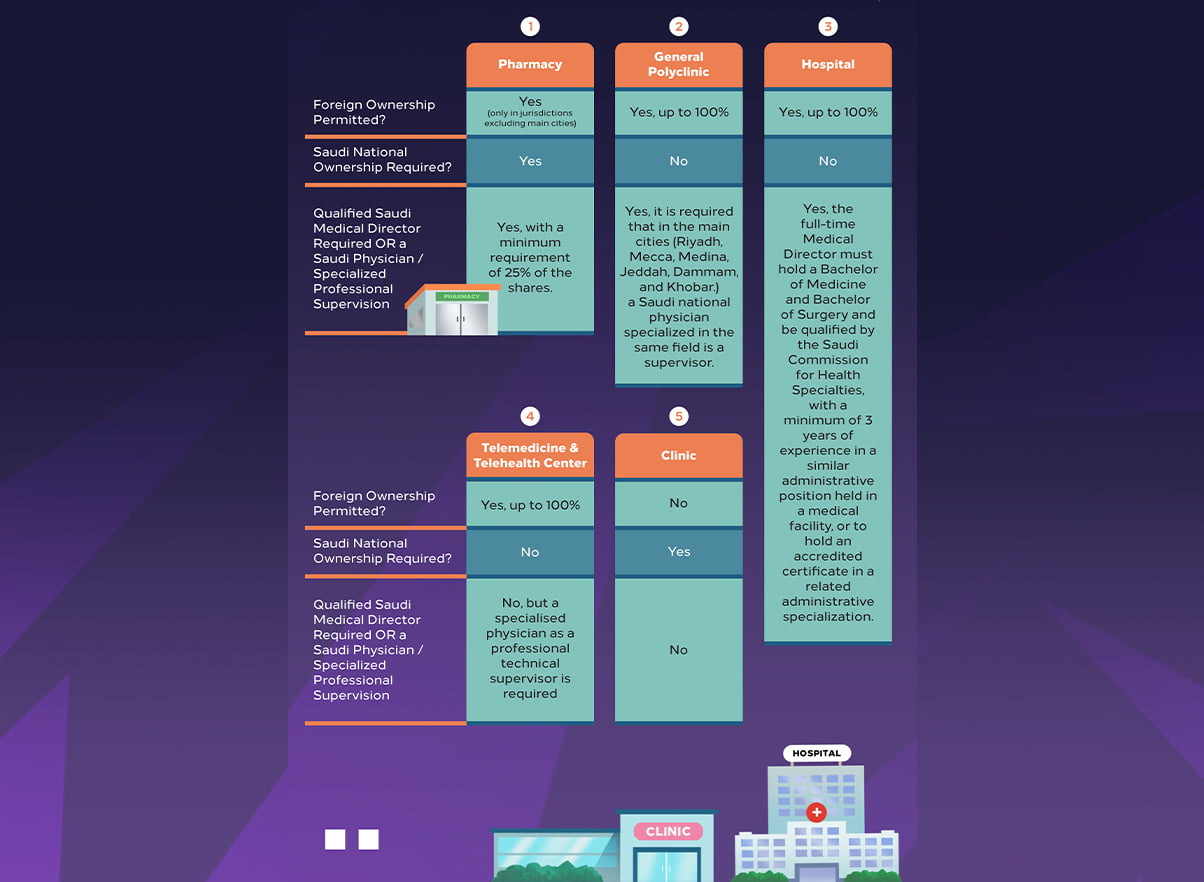

In relation to the healthcare sector, the KSA has also amended its laws and regulations to ease the process of foreign investments within this sector. The illustration explains the basic requirements for investors to establish healthcare entities in KSA.

As per the Vision 2030 initiative and the ongoing updates to KSA laws and regulations, it is now, more than ever, convenient for foreign investors to set-up shop in KSA. We expect continued updates to laws and regulations, and further announcements in the new year, in order to lure in worldwide investments to further positioning KSA as an investment hub in a variety of sectors, including healthcare and life sciences.

For further information, please contact healthcare@tamimi.com.

Published in January 2023